So how would you feel about a stock that pays out a 10% dividend, has the income to cover its dividend, and is a leader in its industry? In a time of 2% 10 year T-Bills, you would guess this is too good to be true. Its not too good to be true – the stock is R.R. Donnelly & Sons (RRD). The one catch: even though its a leader in its industry – its industry is in the slowly melting printed advertising materials. I just started watching this this stock in the last few weeks. I have been wavering back and forth on it, trying to figure out if its a gold mine or a value trap. Here is a breakdown of the analysis I have done:

RRD has two lines of business – Products and Services. According to the companies last quarterly filing, the Company’s product offerings primarily consist of magazines, catalogs, retail inserts, books, directories, direct mail, financial print, forms, labels, statement printing, commercial print, office products and print management. The company’s service offerings primarily consist of logistics, premedia, EDGARrelated and XBRL financial services and certain business outsourcing services.

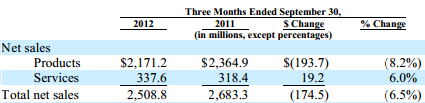

OK, so the service offerings sound kind of interesting – maybe the future of the company. But look – the shrinking products business is 7 times bigger than the growing services business:

Can the company survive long enough to build the service business? Will the print business shrink faster or slower in the future? The company has made a number of interesting acquisitions in the last two years, in both the product and services business:

On September 6, 2012, the Company acquired Express Postal Options International (“XPO”), a provider of international outbound mailing services to pharmaceutical, e-commerce, financial services, information technology, catalog, direct mail and other businesses.

On August 14, 2012, the Company acquired EDGAR Online, a leading provider of disclosure management services, financial data and enterprise risk analytics software and solutions.

On November 21, 2011, the Company acquired StratusGroup, Inc. (“Stratus”), a full service manufacturer of custom pressure sensitive label and paperboard packaging products for health and beauty, food, beverage and other segments.

On September 6, 2011, the Company acquired Genesis Packaging & Design Inc. (“Genesis”), a full service provider of custom packaging, including designing, printing, die cutting, finishing and assembling.

On August 16, 2011, the Company acquired LibreDigital, Inc. (“LibreDigital”), a leading provider of digital content distribution, ereading software, content conversion, data analytics and business intelligence services.

On August 15, 2011, the Company acquired Sequence Personal LLC (“Sequence”), a provider of proprietary software that enables readers to select relevant content to be digitally produced as specialized publications.

On June 21, 2011, the Company acquired Helium, Inc. (“Helium”), an online community offering publishers, catalogers and other customers stock and custom content, as well as a comprehensive range of editorial solutions, in which the Company previously held an equity

Are any of these acquisitions going to be a catalyst for future growth? Edgar Online is an interesting one to me, the others I am not familiar with.

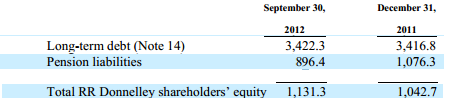

The other big elephant in the room is debt. RR Donnelly has a lot of debt – giving it little wiggle room if things go bad. Check out these numbers from the latest quarterly report:

Thats a Debt Equity ration of 3 to 1, with a big pension liability to boot. Not for the faint of heart – thats about as high as they get.

Conclusion

The latest earnings for RR Donnelly come out on Feb. 26th. I am going to take a look at that before I make any decision on whether to include this in my portfolio. I will be looking closely at the revenue numbers, and if they look reasonably promising, I will likely initiate a small position. It seems reasonable that this stock has a place in a diversified portfolio, as long as you know things could get bad fast if there are any setbacks.