Financial media has been abuzz of late regarding Thursday’s Fed meeting where we find out whether or not the Fed raises the overnight interest rate a quarter point. I am beginning to think this is the Trump-ization of the Fed – much like Trump has brought politics closer to the realm of entertainment – the Fed rate hike is now starting to move into mainstream conversations at the water cooler.

Anyway – Peter Schiff wrote an interesting piece on what I think is more important regarding interest rates – things affecting the long end of the treasury curve (see http://www.europac.com/commentaries/meet_qt_qes_evil_twin).

Remember the Fed can only impact short term rates with rate hikes – to lower long term rates they had to use quantitative easing to aggressively buy mortgage backed securities – thus making it so debt issuers could offer lower rates than they would otherwise because the Fed had their back.

Schiff cites 3 trends which may have a much bigger impact on rates going forward:

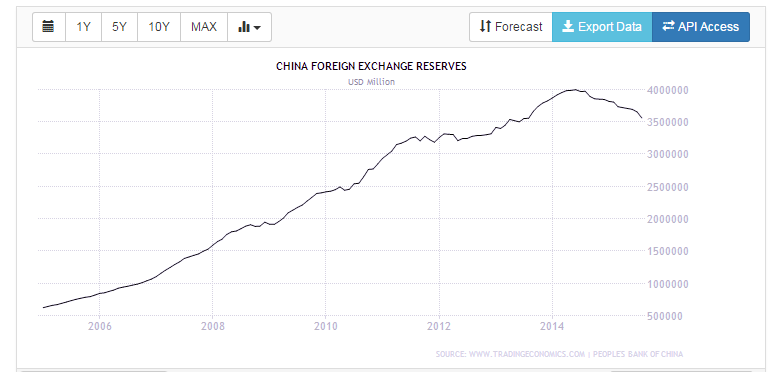

- China has been decreasing its holdings in US Treasuries as their economy slows:

(chart courtesy tradingeconomics.com)

(chart courtesy tradingeconomics.com)

Without the Chinese buying up our treasuries – who will we sell debt to?

- Declining demand from oil rich companies (from Shiff’s article):

The steep fall in the price of oil in late 2014 and 2015 also has led to diminished appetite for Treasuries by oil producing nations like Saudi Arabia, which no longer needed to recycle excess profits into dollars to prevent their currencies from rising on the back of strong oil. The same holds true for nations like Russia, Brazil, Norway and Australia, whose currencies had previously benefited from the rising prices of commodities

- Potential shrinking of the Feds holdings (from Shiff’s article):

Potentially making matters much worse, Janet Yellen has indicated the Fed’s desire to allow its current hoard of Treasurys to mature without rolling them over. The intention is to shrink the Fed’s $4.5 trillion dollar balance sheet back to its pre-crisis level of about $1 trillion.

So with all the potential lack of buyers for all this US debt, whether or not the Fed changes the overnight rate seems pretty inconsequential. I will be listening to hear if the feds plans to stop rolling over it’s maturing treasuries. Or… given the China and Middle East decline in purchases – perhaps the Fed will go the other way, and hint at QE4 (start buying securities again to keep rates from rising)?