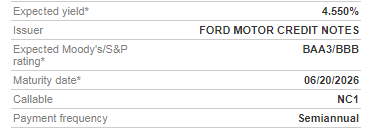

Every once in a while I get a notice of a bond offering from my broker for Ford Motor Credit. As I am always on the lookout for higher yields, I always pause and give this some thought.

With a 7 year CD yielding around 2.0%, my first thought is sure – Ford Motor seems pretty safe, maybe I should go after a higher yield. But after thinking about it a bit more, I always back off.

A couple problems keep creeping back in. First, I think the next market downturn will be initiated by some sort of credit breakdown, whether it be corporate borrowing, consumer borrowing, or sovereign borrowings – all at historically high levels. There is too much debt out there and so I am leery of low rated credit getting rated even lower. If this happens, I either want to be in high quality corporates, or government bonds. I am not sure I can consider Ford Motor a high quality corporation. The stock is lower now that it was 20 years ago, and has a terrible Debt/Free Cash Flow ratio of 6.77.

The second thought I have is the future of car manufacturers. The automobile industry is in the midst of a huge transformation and will likely look quite different in the next few years. From the switch to primarily gas fueled vehicles to electrics, to the concept of ride share replacing car ownership, I think the automobile business model will change drastically.

This disruption will lead to winners and losers. Will the ride share companies running autonomous vehicles be the winners? Will Tesla be the next big car manufacturer? All these questions nag at me as I look over the yield of these Ford Motor Credit bonds.

Investing in high yield bonds is always difficult. Every high yield bond/corporation has its fault, thus the risk premium. In many ways its similar to investing in stocks. It requires an investment thesis and opinion about the future. And for me, a low rated bond focused on consumer credit and the car industry looks like a risk that is too big to bear.