I have been thinking a lot lately about Modern Monetary Theory (MMT) – the economic principle that the US has defacto adopted as part of the COVID-19 stimulus package. One could argue that we had adopted it prior to COVID, but the record money printing that the US did in early 2020 cements our place in the MMT camp.

Can pay for goods, services, and financial assets without a need to collect money in the form of taxes or debt issuance in advance of such purchases;

Cannot be forced to default on debt denominated in its own currency;

Is only limited in its money creation and purchases by inflation, which accelerates once the real resources (labour, capital and natural resources) of the economy are utilized at full employment;

Can control demand-pull inflation[6] by taxation and bond issuance, which remove excess money from circulation (although the political will to do so may not always exist);

Does not need to compete with the private sector for scarce savings by issuing bonds.

So if I understand this right – as long as there is no inflation, the government can print as much money as it wants. Deficits truly don’t matter. I can see why this is so attractive to governments around the world.

A few issues I have with this. It’s pretty clear that as the government has run up huge budget deficits in the last 10 years – the money has gone into the stock market – not the economy. So the only inflation that has occurred is in financial assets, which I assume is excluded from the traditional measure of inflation. Now maybe that is because of the way the government has been distributing all this excess cash. If over the last 10 years the focus had been to to get the money to the public rather than work through the banking system, maybe these excess dollars would be showing up in the economy as inflation.

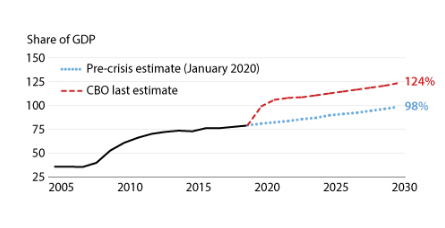

The other issue I have with this (as does the author of these points apparently) is item #4. The assumption is that when inflation does arrive, the government will raise taxes to slow the economy. I find that uh.. very unlikely – as there will be no political will to do so, especially when workers are seeing their paychecks erode during inflationary periods. Unless of course the taxes are raised on financial assets and investments – and we know there is no political will to do that. We can even look so far as the latest CBO Budget estimate to see there is no projection to deal with budget deficits through 2030:

Perhaps the assumption is there will be no inflation for the next 10 years – in that case – the good times are here.

Nobody knows how this will ultimately play out. if no inflation does occur in the next few decades, I will have to admit the Modern monetary theorists were probably right. If we do start to see inflation, and see rising interest rates increase the debt service in our annual budget, I will be interested to see if the Modern Monetary Theorists stick to the plan when it becomes politically difficult.

Adams Resources and Energy is a company I have followed for awhile, and decided to do a deep dive into seeing where this company is going. Right now I am neutral on the stock, but if new management can show commitment to improving margins, it might be a nice ‘safe’ place to invest. Its tied to oil prices, so if you think oil is going to zero (or below) – probably not for you.

When I started this article, my thesis was that the drop in the stock price was justified. But after breaking down the business and looking at the expected revenue contribution of the various segments, I changed my mind.

I am not too wild about any stock in this environment, but I may sell some other stock to raise cash and take a flyer on Townsquare Media.

Microsoft stock has been one of the few stocks I have tracked consistently over the last 30 years. In 1990 I finally decided to buy Microsoft stock, even though the P/E on the stock was through the roof. Previously I had always looked for stocks that appear cheap on a valuation basis, but I felt Microsoft was going to be a winner and it was always overpriced. It turned out to be one of my best investments ever, splitting 7 times from 1991 through 2003.

Microsoft Stock Chart (MSFT)

Unfortunately, I fell in love with the stock and held it throughout the 2000’s when it did very little. The technology world was changing, and the Ballmer administration (in my opinion) lost touch with developers and made some really bad decisions. I finally drained my position in 2010 as I saw no ideas coming out of Microsoft that could justify me owning the position.

After Ballmer left and new CEO Satya Nadella came in, in 2015 I bought a small position since I new Nadella had been the head of the Microsoft Azure Cloud business, where I had seen good and creative decisions. I exited that position in 2016 with a small profit, when I became concerned that the cloud business could not make up for the loss of Windows revenue as the price of Windows goes closer to zero every year. The other concern I had (which I think is still somewhat valid) – is that the cloud business is a commodity business, and all the other cloud providers have alternate sources of revenue. For instance, Amazon and Google could treat the cloud business as a loss leader, really cut the price of cloud, and could survive on its other businesses. Microsoft is disadvantaged in that respect as the Windows revenue is dropping.

But this month, I decided to get back into Microsoft stock. After giving much it much thought I decided that even though it is expensive (much like when I first bought it) I think it has upside potential. Below are the reasons for finally getting back in:

Coronavirus (relative) winner: Long term I think it will gain market share as the S&P 500 companies are forced to retool their workforce for remote work. I think big old companies like that are most likely to default to Microsoft – they likely have Microsoft applications in house, and it would seem to be a comfortable choice. Most companies when they move to the cloud take a ‘lift and shift’ strategy – where they just move applications to the cloud, then retool the applications to run more efficiently and cheaper. During the lift phase of this process, this typically costs more than in-house processing with the promise is long term cost reduction. Microsoft should see profits jump on this shift.

Microsoft Teams vs Zoom: In 2000’s style Microsoft execution, Microsoft inexplicably lost the business video conference war with Zoom. Everybody is using Zoom – when Skype has been around for years. However, I am thinking (hoping?) Microsoft Teams is being improved and has videoconferencing, and should be a better choice for enterprises than Zoom. Maybe this is a Blockbuster vs Netflix analogy – in which case I will be wrong, but I think Microsoft Teams has a decent chance of taking major market share in remote worker productivity.

Augmented Reality(AR) / Virtual Reality(VR): I am beginning to think maybe the enterprise is where AR/VR will take hold and find the ‘sticky’ application that makes it a must have. Maybe with the rise of telecommunication, AR will be the next level on that. Microsoft has done a lot of work on the hololens and if they this technology firmed up and with a good product team, this could be a real growth driver.

Blazor: I have done previous blog posts on Blazor, and the more I work with the more amazed I am with it. It is such a well thought out platform, and I think it will take huge market share from the current in-vogue frameworks like Angular, React, and Vue. It is so easy to get started with , and all the messy Javascript transpiling and packages go away. From a developers point of view its a thing of beauty. Its no coincidence that the development tools work seamlessly with Azure, so as enterprises develop using Blazor and the Microsoft Visual Studio tools, this will make it easier to go with Azure.

So Microsoft is back in the portfolio. In this coronavirus stock market, I am taking the time to improve my portfolio. I sold some other technology stocks to add Microsoft – rather than commit new money to this stock market. I hope I am not too late on this purchase, but it feels comfortable to be back in the Microsoft fold.

I have started to give some thoughts about how to invest in this post coronavirus economic lockdown world, and thinking about how I should adjust my investing thinking in this changed economy. I do think in the next several months to years there will be structural changes in the economy, causing me to rethink my investing priorities. The following is just a sample of my current ideas.

Job automation will be jumpstarted. With demand falling, I think there will be much more emphasis on streamlining operations. Over the last few years we have been inventing technology that has had mild acceptance in corporate america, but now that companies are less fat and happy, they will be up for trying new things.

A couple examples are video conferencing and moving operations to the cloud. Due to the closing of workplaces, video meetings have become a daily requirement for white collar America. As workers become more accustom to this mode of communication, it will lead to improving efficiencies. In addition, having workers work from home will cause employers to rethink management practices as employees are suddenly autonomous. Related to this is moving operations to the cloud – i.e. Microsoft Azure or Amazon AWS. While disruptive at first, this can lead to smoother operations and allow companies to focus more resources on the business and less on infrastructure issues.

Jumpstart to augmented/virtual reality (AR/VR). I know this sounds odd, but for years AR/VR has struggled with mainstream acceptance. This is a technology that is an example where companies have not really figured out how to integrate a technology into their operations. At the same time, the technology is getting better, cheaper and could be more than a niche product. Now that video conferencing and work from home have taken hold, to me a logical extension of this would be VR meetings to better simulate the workplace. These could help the building of corporate teamwork lost when employees are not in one physical place achieving a common goal. Not a big investing theme here for me, but I am starting to think about what technology companies might benefit from the next step up from video conferencing.

Strong Balance Sheets. I have spent a lot of time over the last couple of weeks looking through the balance sheets of the companies in my portfolio. We are in a time where nobody can forecast earnings for the next few months, so looking at the balance sheet and thinking of best case/worst case scenarios helps me assess the near term performance of companies. Those fortunate companies with low debt and lots of cash will be in a good position to ride out any worst case scenarios, and also have the flexibility to pick up low priced assets of failing companies.

Good Management. Good management will be more important than ever for the next few years. My measure of good management will be how well does management adapt to the changing workplace, changing customer demand, and changing supply channels. I think there will be huge opportunities for smart companies to find products in this new environment, and also keep their workforce happy and motivated with new management techniques. Good management may also want to rethink ‘just in time’ inventory approaches, and redesign backup plans for sourcing of materials.

Real Estate Losers. I am very bearish on commerical real estate over the next few years. The triple whammy of a glut of restuarants that will not reopen, an oversupply of hotels for business travel/conventions, and less office space requirements can’t be good. I think smart management will be able to reduce the amount of office space needed per employee. The business convention business has been overlooked as a big loser in this new world. One example is Microsoft cancelled all its in-person events through July of 2021. I have to believe most big business conventions will be cancelled for at least 2020. That’s a lot of empty expensive hotel rooms in the downtowns of many cities.

The Rise of Sports Betting. Another big loser in this event is the hit to municipal economies. With all the revenue shortfall states will incur, I have to believe ramping up revenue from gambling will be an early target. Sports betting was already gaining traction in over a dozen states – I predict wagering on profession sports will be legal in all 50 states by the end of 2021. The winners here will be casino operators.. unfortunately most casino operators have big hotel holdings that will get hurt on the flipside, so choose your investment wisely in this area.

Regardless of whether you agree or disagree with any of the above points, I think its worth it for every investor to envision what the world will look like when we come out of this. Then look at your portfolio, and make sure it is positioned with companies that will thrive in this new environment. Whatever happens in the next few months, I think the stock market will identify big winners and big losers.

As with most people in Washington State, I have been self isolating most this week working from home, and watching the financial headlines roll through like thunderstorms. I have spent so much time in my office chair this week I am looking for backup chairs in case my main steed fails.

This market drop and has been sudden and spectacular. Record breaking volitility, massive economic shutdowns, and pandemic fears make data driven investing extremely difficult. I have been asked by several friends over the last few days for market opinions, and gladly respond to anybody who cares to hear my amateur-status opinion. In past months, you could have looked at invest.vfsystems.net to get my rough view of the market, but in this enviroment, its moving too fast for that data-view of the world. So please feel free to email me any time you have market questions – I am full of free advice and opinions.

In summary, I do believe this will be a more significant event that the 2008/09 great recession. The worldwide supply and demand shock in this highly levered world is going to cause severe economic damage and change. Perhaps this quote from Warren Buffet is the most appropriate now:

Only when the tide goes out do you discover who’s been swimming naked.

The tide went out very quick in this case, and indeed, a lot of companies are scantily dressed (I am looking at you Boeing).

Having said all that, I thought I would post these thoughts, giving you an overview of what I have seen this last few weeks and what I am thinking:

GDP Estimates – It was fascinating to watch the GDP estimate revisions for 2020 come out this week. On Monday, Goldman Sachs forecast a 5% drop in Q2 GDP, then a 4% rise in Q3 GDP. When I saw that I knew that was still way too optimistic. As of this writing at the end of the week, Goldman is now down to -24% (!) Q2GDP and looking negative all year:

Ouch!

To be fair – nobody knows – past data is pretty much useless now, so everybody is just guessing. But it cant be good.

The Speed of the Market Drop – Speaking of data, the speed of this drop is what was most unique about this downdraft. My investment models look at economic data and predict expected prices based on that data. We have no precedent for such a sudden global economic stoppage. And the economic data we have is in many cases too old. For instance, Housing Start data came out on Wednesday this week, and the survey was for February, which by now is ancient history. The number was down slightly from the all time high. Typically Housing start data has been a good predictor of slowdowns, but because of the speed of news we wont see Housing start data tank until we get the March numbers in late April. So I have some work to do to figure out how to get more timely data or otherwise deal with fast moving markets.

Investing By Hand – Because the market is moving faster than my data, I took my investing strategy off autopilot, and am now investing largely on untested theories and headlines in this turbulent market. This is extremely dangerous. However, I am working to repair my models, and every day I think I get better data to help drive decisions in this new environment. I am gravitating to strong companies I know, with smart management. Going into this crash I was fairly defensively positioned, and as this market has dropped, I have gotten more defensive. My model is still fairly positive on the market, but again, the lack of timely data makes that opinion near worthless. The most important thing is to keep my emotions in check and look at the data coming in rationally.

Bet Against Commercial Real Estate – One non-data related trade I made was to by a Sept 2020 70 strike price put on the VNQ. The VNQ is the Vanguard REIT Index. This was a trade I had been thinking about, but was triggered largely by the news that our local high end mall was closing for two weeks. This mall, like many malls, has been increasingly opening restaurants in place of stores closing due to the retail apocalypse. As the coronavirus hit, all the stores and restaurants immediately emptied out. When this local mall closed, it was enough for me to act on my thesis that the impact to commercial real estate will be devastating from this point forward. We already had too many restaurants opening. We had massive building of commercial offices built downtown (now and in the future to be empty due to working from home). Finally, in our town we have had thousands of new hotel rooms built in high rise hotels built in the last couple years alone. I am confident in the next few months, we will find out which hotel chains have been swimming naked.

Regarding working from home, yes I think people will return to offices after all this. This event has caused me to use on a regular basis teleconferencing software, and I must admit, it works pretty well and once a home office is set up, you can be at least nearly as productive as in the office. I think businesses can adapt to this new paradigm on an ongoing basis. Yes I believe employees still need central meetings periodically, But I think this will kick off a large shift of offsite rotation. Maybe this will lead companies to reducing office space needs by 1/3? If so, that is a lot of nice empty office buildings.

In summary, I do not think this market drop is over. In 2008/09, the market dropped by ~55% peak to trough, and as of this writing we are down ~32%. I see no reason why we shouldn’t drop less than ~55%, and I think there are a lot of bad headlines coming our way in the next few weeks.

With the lack of data, I think many people are having to invest on emotion. I was talking with a neighbor, and we agreed at this point it may best to close the markets for a couple weeks because of the trillions of dollars being traded purely on headlines and emotion. Lets take a couple weeks to gather data, get a bearing on the economy, then re-open the markets. Maybe that’s not possible with global markets, but I feel that would help.

Regardless of the Coronavirus’s ultimate health toll, I don’t see this as a quick economic recovery. With a 2020 government deficit now projected to be over 3 trillion after all the stimulus being discussed, I think the economic impact of this event will last for years. In the coming days, we will see many corporate losers, surprise bankruptcies, as well as a few winners in this new digital economy. And I still don’t think we are near the market bottom.

One of the most under-reported economic stories of 2019 was the problems with the Repo Market and ‘Not QE’. This article does as good as job of any as explaining whats going on. This is a complicated topic, which is why it hasn’t been covered outside of the financial press, but it seems to me this will have huge implications in the coming years.

Starting in October, largely due to all the government securities being issues, the Fed stepped in and became a net buyer of Treasury securities. Wall Street & the banks treat treasury securities like liquid assets – the problem now being there are so many treasury securities in the market, the appetite is dwindling. Banks are stuffed with treasury securities, foreign interest is stalled. It seems everyone who wants to own a treasury bill has one.

Prior to this, starting in late 2017, the Fed had been (slowly) trying to drain off all the debt it added over the last 10 years. One could argue this was a major factor in the stock market ending down in 2018, with its low in December when the Fed raised rates, and signaled more to come in 2019. In January, the Fed reversed course and signaled lower rates, juicing the stock market to new highs. Now that the Federal Reserve is keeping rates low, they added fuel to the fire by injecting (printing) more money into the system, which has the effect of ending up in the stock market directly. It would seem this is what might be fueling the recent highs in the market.

Another longer term ticking time bomb is all the retirement assets accumulated by baby boomers. As boomers quit accumulating wealth (or die), and they become net sellers of financial assets, that money will be passed back into the economy, flooding the economy with all these T-bills that have been hoarded in these retirement funds. I think this may finally lead to the inflation that has been long predicted by economists when government runs large deficits. Once that money leaves the hands of old savers, and into younger spenders, a lot more money will be chasing the same goods which is a recipe for inflation.

Historical economic theory would assume that rising federal debt would lead to higher interest rates, as supply of debt exceeds demand. So far that hasn’t happened. I think this has been distorted by the huge Baby Boomer appetite for savings, and recent Fed policy is distorting markets by ‘hiding’ this debt on the balance sheet. And because it appears to the public and politicians that ‘deficits don’t matter’, there is no appetite to reign in all the federal debt. So far, its working. But I believe deficits do matter. How long the government can continue to print paper to cover these debts is anybody’s guess. At some point one can assume markets will care? And what will happen when markets do care? That is a question that will be have to be answered sooner or later.

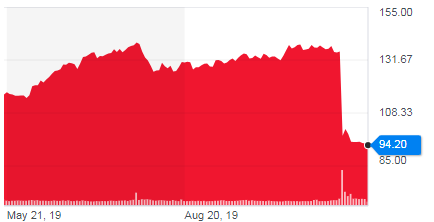

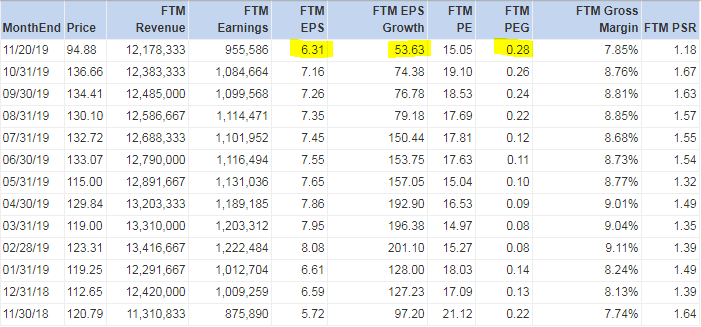

In September I made an ill-timed move into Expedia stock, just in time to see the stock drop by 30% in November. The drop was primarily due to a bad earnings release – revenue number lower than expected and and EPS miss by $0.43 a share. In addition, the market is spooked by Google getting into the vacation rentals space in this already competitive environment.

So what to do now? Do I bail or buy on the dip? Arguably, its too late to bail on the stock:

6 month Expedia stock price

So I need to see if it makes sense to add to my position – because if I liked it at $132 I should love it at $94. Looking at the forward estimates does’t paint a great picture:

For the last year for Forward Twelve Month estimates (FTM) have been consistently dropping, at even after the drop the forward price earnings growth (PEG) metric is historically high. So that explains the nervousness about the stock.

However, if you believe the nervousness that Google will keep squeezing Expedia is overdone, and they can stabilize EPS growth, I think there is some opportunity here. Short term I think the drop is overdone. This is still a stock that is growing earnings at 50% per year, with a PE below market. Not that I am super bullish on this stock long term, I just think its OK to play for a bounce on this. So in my case, I added to my position in late November to get by cost basis break-even lower. I think this will be a short term (1-2 month) trade, with the assumption that I will lighten up on my Expedia holdings after a month or so, and take the short term tax loss on my initial purchase. My valuation and technical model is positive on this stock for the month of December, so I would guess the majority of the bounce will happen in the next 30 days. After that, I will have to wait and see because my model doesnt forecast past 30 days.

Long term, I am not sold that Expedia will dominate the travel world, but I think its worth a 30 day trade to assume that everybody who was going to sell has already sold.

The recent 2020 campaign discussions on billionaire taxation are bringing about an interesting discourse, but I wish someone would bring up problems with current philanthropy rules. It seems to me an easy step for someone to take would be to tighten the loopholes of big charitable giving.

This article does a great job discussing The Perils of Billionairre Philanthropy. It seems to me that charitable giving has surreptitiously become primarily a tax avoidance tool for the wealthy. A great stat from this article:

In the early 2000s, households earning $200,000 or more made 30 percent of all charitable deductions. By 2017, this high-earner group accounted for 52 percent of donations. And the total share of charitable deductions from households making over $1 million dollars grew from 12 percent in 1995 to 30 percent in 2015, according to IRS data.

Why the change? A couple reasons in my opinion.

Donation of appreciated stock. A hidden gem of tax avoidance for anybody who has stock that has greatly appreciated. When you donate stock to charity, you get to take the charitable donation credit on the full value of the stock, without taking the capital gain. A couple great examples here. Bill Gates donated $4.6 billion dollars of stock to his foundation in 2017 without paying any capital gains. Lets assume his cost basis on that stock is near zero, and he is in the tax bracket that would pay 20% capital gains tax. By doing this, he was able to avoid paying roughly $920 million in capital gains in 2017. In 2018, Warren Buffet donated 3.6 billion in stock to the Bill and Melinda Gates foundation. Using the same math, I count that as $520 million avoided in capital gains taxes. That’s $1.5 billion in lost taxes in these two examples alone. Yes the money goes to philanthropic ventures, but is that equitable? Now.. it is a pain to donate stock to charity.. which leads me to #2.

The rise in Donor Advised Funds. Donor advised funds are a great tool to give to charity for the wealthy (and upper middle class) to get a tax break. The game here is instead of giving directly to charity every year, every few years to give a lump sum to a Donor advised fund, which is essentially a pool of charitable money that can then be distributed to a different charity at any time. By giving a lump sum, people who do not hit the threshhold for itemizing their taxes can now get a charitable tax break. An Example: Lets say a married couple earns $16000 in taxes, and gave $3000 in charitable gifts in a year. Given the standard deduction is over $20k it makes sense to just take the standard deduction and not take itemized deductions, thus losing your charitable deduction. However, if instead of giving $3k to charity every year, you give $15000 to a Donor advised fund every 5 years. This gives you a $12,000 write-off every 5 years for charitable contributions because you can itemize that lump sum every 5 years. The kicker of course is, if you have appreciated stock, you can contribute your appreciated stock (see #1 above) to the fund to further leverage your contribution and take advantage of tax rules. Then, thoughout the year you dole out your money to your favorite charities from your balance in your Donor Advised Fund. These funds are very easy to set up and use – but how many people can take advantage of them?

It occurred to me that companies that have a 401k must follow strict IRS guidelines to ensure their plan is equitable by ensuring employees participate from all income levels. These charitable donation loopholes have been around for years, so they likely have bipartisan support because they encourage charitable giving. But how hard would it be to look at the above issues to make them equitable? Either change the rules to either cap tax free contributions, or change the rules so people from all income levels can take advantage of these tools.

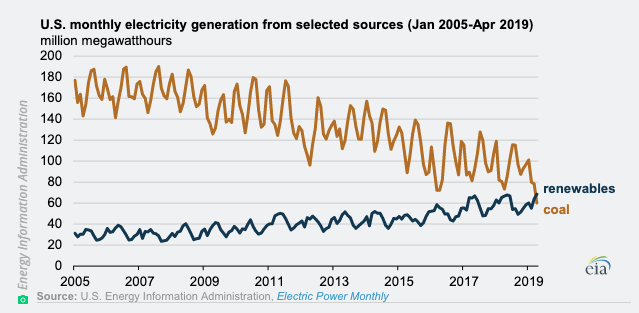

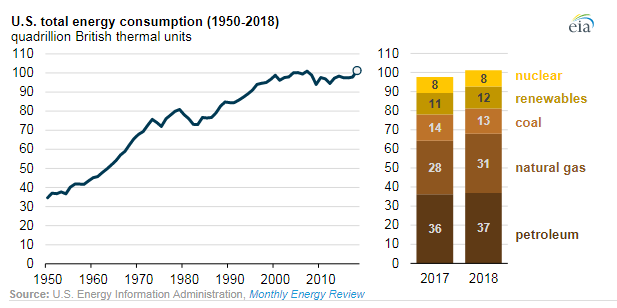

This chart from the US Energy Information Administration also shows an interesting chart – total US energy usage, while up in 2018, has been relatively flat since the mid 2000’s:

Given the rising market share, and the aging of the US population, it seems that petroleum share will have to start shrinking. The primary reason its share has been rising is the dramatic fall in oil prices since 2010. The price of crude oil is now roughly just over half of what it was in between 2010 and 2014. One would think that with the advances in Solar and Wind power lowering the costs of electricity, petroleum prices will have to continue to fall in order to maintain market share.