I recently had an article published on SeekingAlpha.com with my read on Nordstrom’s Fourth Quarter Earnings. Check out the article at

http://seekingalpha.com/article/1225391-what-i-liked-about-nordstrom-s-q4-earnings

I recently had an article published on SeekingAlpha.com with my read on Nordstrom’s Fourth Quarter Earnings. Check out the article at

http://seekingalpha.com/article/1225391-what-i-liked-about-nordstrom-s-q4-earnings

I was reading an interesting post at www.whowhatwhy.com regarding Barrett Brown – another internet ‘hacktivist’ in the mold of Aaron Schwartz. Brown has been in custody since September 12th, 2012, on ‘charges of threatening a federal officer’. Interestingly, according to this post, what the government was really after was to shut down his site which was designed to collect user contributed information to connect the dots behind the Stratford emails leaked by Wikileaks.

Anyway, the paragraph that particularly caught my attention was this:

With much ado in recent days about Chinese cyber espionage, the government is using this new “Yellow Peril” as an opportunity to mount a full court press against the ability of any group to maneuver on the Internet in ways that might threaten corporate and state interests.

So it got me wondering about that – so I did a little googling on this whole Chinese cyber espionage stuff we have been hearing so much about. It turns out the driver of all this news is a report released by the Mandiant Corporation. First off – where do you suppose Mandiant Corporation is headquartered – yep – Alexandria, Virginia. A little suprising that a big independant security firm serving Fortune 100 clients wouldnt be located in Manhattan, or Silicon Valley – but maybe its just a coincidence.. I also wondered what the motive would be for a security firm to make a big splash about calling out the Chinese for hacking. Wouldnt it be in the best interest of security to lay low and gather as much information about them before tipping them off that you are on to them? Maybe it is just a publicity move, but it fits in nicely with the administration’s (and Congress’s) efforts to clamp down on internet freedom in the name of national security.

Finally, this article on comparing Mandiant to Blackwater had a couple interesting points:

The report, embraced by stakeholders in both government and industry, represented a notable alignment of interests in Washington: The Obama administration has pressed for new evidence of Chinese hacking that it can leverage in diplomatic talks — without revealing secrets about its own hacking investigations — and Mandiant makes headlines with its sensational revelations.

and

Mandiant’s staff is stocked with retired intelligence and law enforcement agents who specialize in computer forensics and promise their clients confidentiality and control over the investigation. In turn, they get unfettered access to the crime scene and resources to fix the problem (Mandiant won’t say exactly how much it charges, but it’s estimated to average around $400 an hour).

So, a security company located in inside the Washington DC beltway, stuffed with former intelligence agents, partnering with Fortune 100 clients. Nothing suspicious here…

All I ask is that the next time a story comes out regarding cyber crime, see if it parallels the ‘War on Terror’ storyline. And watch to see what additional restrictions on civil liberties are proposed to protect us from these new ‘terrible threats’.

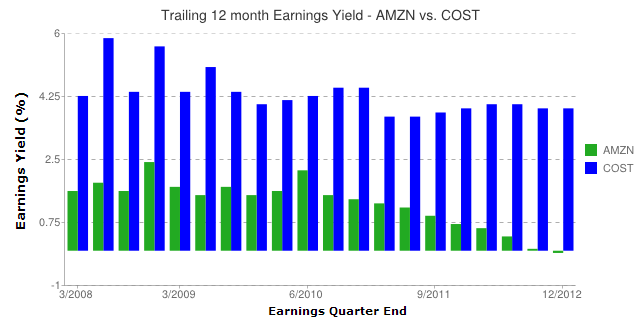

Amazon is a tough stock for a value investor like me to own – it has always been overvalued. Yet it has been a great stock for years – up over 10 times over 10 years. It currently is a $270 stock, with a negative 12 months earnings. Compare that to Google – $800 stock with $32 in annual earnings, or even a Costco – a $100 stock with $4 in trailing 12 month earnings.

I decided to run some comparisons of Amazon with Costco – somewhat similar retail presence, leaders in their field, and likely to thrive in the new internet-centric economy. First, take a look at this earnings yield comparison:

It doesnt alarm me that their earnings yield has gone negative – Amazon has always been running on tight margins, investing in growth. They are pumping lots of money into new distribution centers in many states to allow for quicker and cheaper shipping to more destinations. However the 18 month trend of shrinking yield – caused largely by the stock price runup, has me a little worried – and when compared to a solid company like Costco, they have a lot of ground to make up.

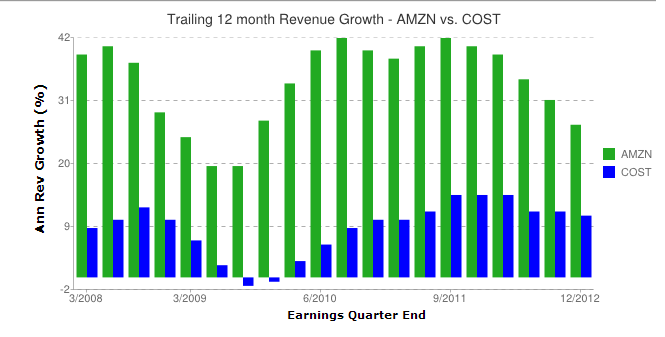

The other chart that bothers me a little more is the revenue growth chart:

Revenue growth has been shrinking – perhaps the new distribution centers will help, but you have to wonder if the glory days of Amazon’s growth is behind it. The market certainly doesn’t think so – during this time Amazon has quadrupled:

As much as I like Amazon the company and its future prospects, at this point I think I can find better long term value in the stock market. Its tough to bet against this stock – its always proven doubters wrong, but maybe this time its time to get out.

So how would you feel about a stock that pays out a 10% dividend, has the income to cover its dividend, and is a leader in its industry? In a time of 2% 10 year T-Bills, you would guess this is too good to be true. Its not too good to be true – the stock is R.R. Donnelly & Sons (RRD). The one catch: even though its a leader in its industry – its industry is in the slowly melting printed advertising materials. I just started watching this this stock in the last few weeks. I have been wavering back and forth on it, trying to figure out if its a gold mine or a value trap. Here is a breakdown of the analysis I have done:

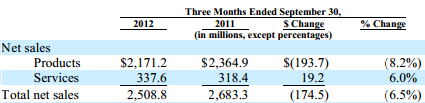

RRD has two lines of business – Products and Services. According to the companies last quarterly filing, the Company’s product offerings primarily consist of magazines, catalogs, retail inserts, books, directories, direct mail, financial print, forms, labels, statement printing, commercial print, office products and print management. The company’s service offerings primarily consist of logistics, premedia, EDGARrelated and XBRL financial services and certain business outsourcing services.

OK, so the service offerings sound kind of interesting – maybe the future of the company. But look – the shrinking products business is 7 times bigger than the growing services business:

Can the company survive long enough to build the service business? Will the print business shrink faster or slower in the future? The company has made a number of interesting acquisitions in the last two years, in both the product and services business:

On September 6, 2012, the Company acquired Express Postal Options International (“XPO”), a provider of international outbound mailing services to pharmaceutical, e-commerce, financial services, information technology, catalog, direct mail and other businesses.

On August 14, 2012, the Company acquired EDGAR Online, a leading provider of disclosure management services, financial data and enterprise risk analytics software and solutions.

On November 21, 2011, the Company acquired StratusGroup, Inc. (“Stratus”), a full service manufacturer of custom pressure sensitive label and paperboard packaging products for health and beauty, food, beverage and other segments.

On September 6, 2011, the Company acquired Genesis Packaging & Design Inc. (“Genesis”), a full service provider of custom packaging, including designing, printing, die cutting, finishing and assembling.

On August 16, 2011, the Company acquired LibreDigital, Inc. (“LibreDigital”), a leading provider of digital content distribution, ereading software, content conversion, data analytics and business intelligence services.

On August 15, 2011, the Company acquired Sequence Personal LLC (“Sequence”), a provider of proprietary software that enables readers to select relevant content to be digitally produced as specialized publications.

On June 21, 2011, the Company acquired Helium, Inc. (“Helium”), an online community offering publishers, catalogers and other customers stock and custom content, as well as a comprehensive range of editorial solutions, in which the Company previously held an equity

Are any of these acquisitions going to be a catalyst for future growth? Edgar Online is an interesting one to me, the others I am not familiar with.

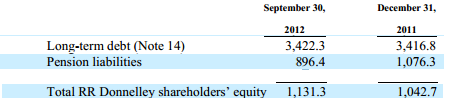

The other big elephant in the room is debt. RR Donnelly has a lot of debt – giving it little wiggle room if things go bad. Check out these numbers from the latest quarterly report:

Thats a Debt Equity ration of 3 to 1, with a big pension liability to boot. Not for the faint of heart – thats about as high as they get.

The latest earnings for RR Donnelly come out on Feb. 26th. I am going to take a look at that before I make any decision on whether to include this in my portfolio. I will be looking closely at the revenue numbers, and if they look reasonably promising, I will likely initiate a small position. It seems reasonable that this stock has a place in a diversified portfolio, as long as you know things could get bad fast if there are any setbacks.

The rules for Drone strikes are now out, and they show the same disregard for the constitution as the torture framework created under the Bush administration.

http://www.bbc.co.uk/news/world-21333570

The part that I find most disturbing is the legal framework for using lethal force against US Citizens. I lifted this paragraph from the leaked memo:

“the United States would be able to use lethal force agains a US citizen, who is located outside the United States and is an operational leader continually planning attacks against US Persons and interests, in at least the following circumstances: (1) where an informed, high-level official of the US government has determined that the targeted individual poses an imminent threat of violent attack against the United States;(2) where a capture operation would be infeasible–and where those conducting the operation continue to monitor whether capture becomes feasible; and (3) where such an operation would be conducted consistent with applicable law of war principles.”

Incredibly, this paragraph is followed by a total disclaimer of constitutional principles:

The condition that an operational leader presents an ‘imminent’ threat to violent attack against the United States does not require the United States to have clear evidence that a specific attack on US persons and interests will take place in the immediate future.”

This framework centers around the killing of Anwar al-Awlaki – a US citizen that was droned in 2011. Interestingly, even if you believed we had the right to kill anybody using the rules defined above, the argument that Anwar al-Awlaki meets these criteria is weak.

Al-Awlaki was targeted because he was a radical Islamist speaker and spiritual leader – he was not an ‘operational leader’. If you read his Wikipedia entry (http://en.wikipedia.org/wiki/Anwar_al-Awlaki), it’s not even conclusive he was a member of al-Quaida. And no proof has been provided by the government that he himself ‘posed an imminent threat of violent attack against the US’.

Punishment for imminent lawless action has been defined by the Supreme Court in the Brandenburg vs Ohio case. In reading that case, it doesn’t seem to me there was proof of an ‘imminent threat’ – not to mention that the penalty al-Awlaki paid was death, and without due process.

Because there is no constitutional basis for this, the statements in the memo mean lethal force could be stretched to apply to any political activist, speaker or author critical of the United States – depending on the how the government defines ‘violent attack’. If history is any guide look for this framework to be loosened and expanded by subsequent administrations. Torture was re-legitimized in the 21st century in the name of national defense, and has been expanded to American citizens accused of crimes against the state. Worse yet, this lethal force is being administered and committed not by a police force or the Defense department, but by the CIA – a department with limited governmental oversight and near zero public scrutiny.

Death to American citizens by executive order has been justified, without debate or review by either the judicial or legislative branch. This is truly a sad day in American history, and unfortunately only the beginning.

If you are still of the belief that Boards of Directors have the best interest of their shareholders in mind – I have bad news for you. Footnoted.org has a great example of Corporate malfeasance perpetrated by the CEO and the Board.

http://www.footnoted.com/buried-treasure/too-early-for-worst-footnote-of-2013/

The board of directors has bestowed a gift to the outgoing Executive Chairman- I am sure it was meant as a nice gesture. In doing a little math, If you owned 100 shares of Apollo Group, worth about $2,000 as of this writing, that gift the board bestowed cost you approximately $5, and about $.75 a year to the uh…, less than needy recipient.

I am sure the board sensed the shareholders of the company would feel just as charitable, because any shareholder of the company over the last 5 years have given away more than that by just owning the stock. Seeing as the outgoing Executive Chairman holds over $200 million in Apollo stock, I guess everyone can understand why he deserves such a heartfelt gift.