This interview with Mohamed El-Erien has a great quote in it which got me to realize why I find economics so interesting:

In the mid-’80s the IMF made an attempt to understand financial markets. And I was sent to talk to asset managers in New York. The question was asked to them: “What was the first thing you did when you heard Mexico wouldn’t be able to meet its debt repayments?” — which happened in 1982. And the asset manager said, “I sold Chile.” To an economist, this made no sense. Chile was a very well-managed economy; it never had to restructure. So the economist in me thought, “Wow, this is a difficult, irrational market participant.” But he explained, “Look, I manage Latin American funds, I believed, and it turned out to be the case, that some of my investors, when they read about Mexico, would take their money out of the fund. I didn’t want to be left with an over-concentrated position so I got ahead of that trend by selling Chile and some other winners.” And I remember being amazed that there was this whole other dimension out there that goes beyond economics and policy, and it goes back to the idea that how you think about things is very important.

Like the game of chess – economists have to think a few moves ahead to visualize the future. Predicting the future is fraught with error, which is why so many smart economists see a wide variety of futures.

So when I hear about how the world is overleveraged in a declining growth environment, and this portends bad news for the future, I have been trying to make sense of who the world winners and losers will be. One of my favorite sites for this is tradingeconomics.com where you can easily see world economics to try to understand bond valuations.

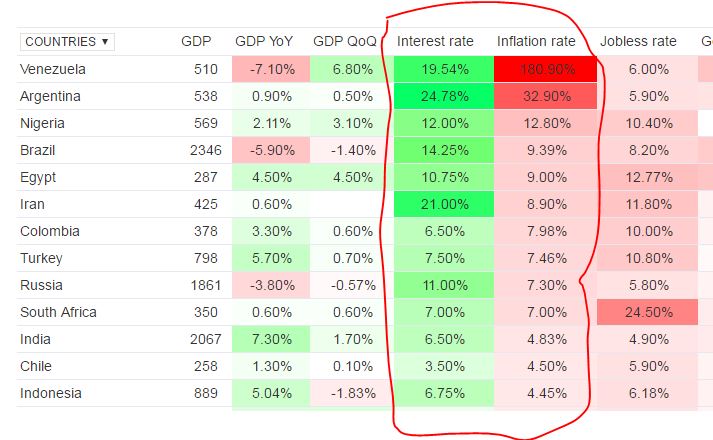

Lets first look at how world interest rates appear to be determined. By looking at this chart below, it appears to be highly correlated to the countries inflation rate:

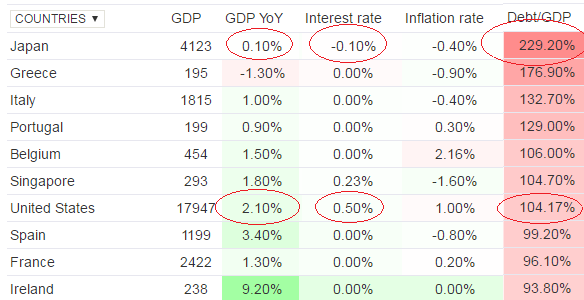

But if you want to look at the potential for government debt default, wouldn’t you think that countries with high debt to GDP would have higher interest rates as a reflection of the debt default? Not so:

Japan, with the highest debt to GDP, and lowest GDP Growth, has the lowest interest rate. Looking at this chart, why would anybody own Japanese debt instruments? While its sad to see the US in the top 10 of this list, arguably it is the safest bet – highest GDP growth, highest interest rate, and (relatively) high inflation rate – which is important for highly leveraged companies to inflate their way out of debt.

I think current world bond pricing is ignoring soverign debt default risk, and I can’t explain it. If fact, when the Brexit results came in, Japanese Yields went down as investors switch to Japan in a flight to safety. So I don’t get it, but I do think markets will correct and debt quality will become a factor in bond pricing. And when this happens, world markets will be in turmoil.