Lots of articles have been written about the ridiculousness of NFT’s (Non Fungible Tokens) and examples of outrageous amounts being paid to ‘own’ digital items. While I agree that the amount that some people are paying for NFTs are head-scratching, I think there is a place for NFT’s in the future.

Here is a good overview article on NFT’s. I think we are early in this trend, and while it is in the experimental phase I think alot of crazy things will be bought and sold. But conceptually, NFT’s do have advantages over physical collectables. People buy collectibles because they like having the items around them, and they hope that someone else will find them more valuable in the future. The same is true of NFTs. Except with NFT’s, you don’t need to worry about accidental destruction of your collectible, dedicate a room to house all that stuff, or insure it. Some might say they want to physically touch the collectible, but for the most expensive ones, you can’t since that could cause wear and tear and reduce the value. I addition, any NFT that has an official registry can guarantee you have the authentic ownership – where as a physical asset may be a forgery or a copy.

One knock on NFT’s is the lack of scarcity – and how people are just putting all sorts of things up for sale. That is not unique to NFT’s – the amount of physical collectibles out there are seemingly unlimited – from movie franchises, artwork, coins, furniture, just about anything. Anything that someone thinks might be worth more in the future.

So once the hype phase and headlines die down on these NFT’s that are being sold I think someone will find a model that makes for sensible NFT collecting. I think the NBA has an interesting model with it’s top-shot collection. One old school NFT is domain name collecting – people don’t think of that as NFT’s, but what are you really buying when you buy a domain name. Once scarcity in a digital item can be defined, it is a candidate for collecting.

One other interesting model is Earth2.io. This is quite interesting to me – because it has a defined scarcity of elements you can buy (grids on planet earth), and because people seem to be paying a lot of money for these grids. I could spend money on their site to buy the 3 or 4 grids of my house location for around $300 bucks. The reason I would do that is to stake my claim on earth2, and believe that my investment would be worth more in the future. If earth2 can build into something that catches popular culture’s imagination and becomes the most talked about investment since crypto – then that seems like a great investment. But this is just one of many NFT models out there, and so whether it amounts to anything or not will be interesting to watch. As interesting as I find Earth2.. I have no plans to buy land.

I will keep being amused by all the crazy things that people are selling and buying in the NFT world, as it makes for great stories. But long term I do believe there is something to NFT’s as a collectible and a store of value. Maybe even more so than crypto currency, which lacks the collectible aspect of an ‘asset’. I will be keeping my eye out for the NFT that I think has the right model, and maybe then I will join the world of digital collectables.

I finally built a position in Apple stock after years of being out of it. The last time I held Apple was in 2013, but I sold out based on just not being a believer in the company. I was not impressed with their ability to innovate, and I didn’t think their app store margins could hold up, so I thought there were better opportunities elsewhere.

For the most part – I was wrong.

I will admit that it has been hard to match the performance of the S&P 500 without holding any Apple stock. Apple accounts for around 5% of the S&P 500 – so I have been missing an important factor in my quest to beat the S&P.

I am not in the Apple ecosystem – the only Apple product in our house is my spouse’s work phone. But I am seeing a few reasons to buy the stock now – which is what let to my change of heart:

A Bond Proxy. As mentioned in previous posts, holding bonds seems like a no-win situation. I don’t see rates falling much more, so the only thing they can do is stay flat or go up. When rates go up, bond prices fall because old bonds are less attractive than new bonds issued at higher interest rates. So if rates stay flat, Apple’s yield pretty much matches a bond’s interest rate. And if rates go up, I think Apple will be hurt less by higher rates than bonds. Yes Apple is overpriced currently on a historical basis, and it could drop if rates go up, but long term I think its a better bet than bonds. I have a hard time seeing Apple stock being lower in 10 years, than bond rates being lower in 10 years.

Apples New Chipsets. There has been alot of hype around Apples new M-1 chip, which perhaps is overdone, but I think the chip is still a huge improvement over Intel’s offerings. I am in the camp that the the sun setting on Intel’s x86 architecture, and Apple is has made a big step away from that. In addition, with Microsoft looking at Windows for ARM, and servers switching to ARM from x86, I think Apple has taken a lead in the movement, and will draw market share short term in the PC market until (unless) PC’s migrate to an architecture as performant as the M1.

Augmented Reality. As mentioned in a previous post, Apple is moving into Augment Reality and possibly Virtual Reality (AR/VR). I mentioned that I think the lack of progress in AR/VR is a product problem, not a technology problem, and I do think Apple with its strong ecosystem has a decent shot of building something to really be the next generation device. If so, it will power upgrades across all their hardware offerings.

Other new devices. Apple is only strengthening their ecosystem with well designed products. I was skeptical that Apple could build the watch business, but I think I was wrong about that. This week they announced their new Air-tags, which I think are a compelling offering, and they are making real progress with home automation with improvements to Homekit. One problem with home automation is the complexity of setting up devices and all the different apps and ecosystems – and Apple has the ecosystem that is stronger than all the others.

I still am skeptical that Apple can keep their 30% margins in the app store – we have already seen them start to weaken on their pricing. But at this point – I think they have enough new products to build their ecosystem and user base to offset any margin shrinkage. I had also been skeptical that Apple was not much of an innovator – every year they just add silly bells and whistles to their phones to get people to upgrade. But I am seeing enough evidence now that they have been doing a great job innovating all their products into an ecosystem, with a real vision on how it will all fit together.

I hate buying stocks like this after a long huge runup, but I am not looking for this new stock position to ‘knock it out of the park’. Apple will be just a core position that I hold and hopefully just watch it grow slowly, as the company sucks more and more people into their ecosystem. I still have no plans to buy any Apple products.. but never say never.

I finally broke down and bought some crypto currency. While I was never in the camp that crypto was a fad, I was never a believer enough to actually buy any. What finally tipped the scale for me was seeing all this big money going into bitcoin. More and more big Wall Street money managers are hedging using crypto, and soon you will see ETF’s available which will make it much more easy to buy and liquid. So finally, I bought a tiny enough so at least I can get a better feel for where crypto fits in my investment portfolio.

First I had to decide on a crypto coin. I finally decided to buy Ethereum – not Bitcoin.

I bought Ethereum not because I know what I am doing, I just weighed a few factors:

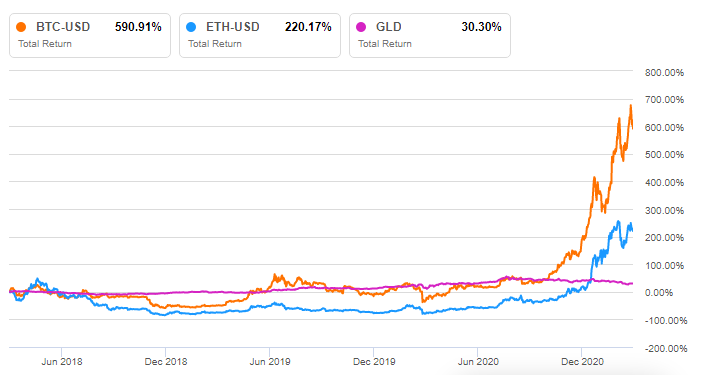

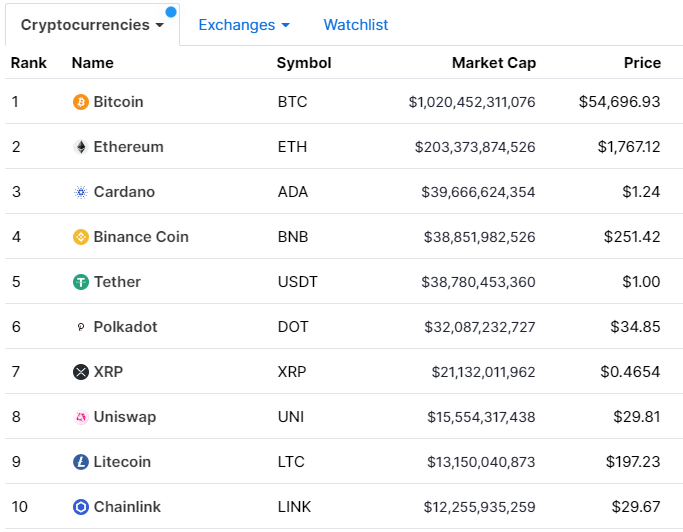

First, I wanted a coin with one of the top market caps. There are a zillion different crypto currencies, and the only ones that are valuable are the ones that people think are valuable. The bigger a market cap gets, the more it represents trust. Here is a chart of the top 10 cryptos ranked by Market Cap:

Second, I noticed that non-fungible tokens (NFT)’s primarily trade in Ethereum. Now that NFT’s are here – crypto currencies are starting to look pretty mainstream. I am not a believer in NFT’s enough to consider buying any, but I do think its an interesting concept – more on that in a future post.

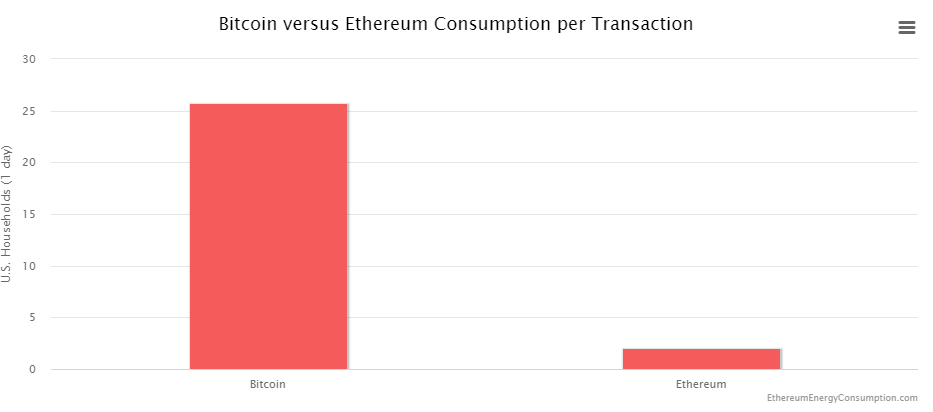

Bitcoin gets a bad rap because of the energy it takes to process transactions, and indeed it is much more energy heavy:

I assume if Ethereum reaches the scale of bitcoin the energy usage will rise to match, but Ethereum does have on its technology roadmap a plan to make it much more energy efficient. While Ethereum has not performed as well as Bitcoin as seen by the chart above, it tracks it close enough for me until I have a better idea of what my strategy is.

Note also from the chart above how both Bitcoin and Ethereum have performed as compared with Gold (GLD). One would think Gold would somewhat match the chart of crypto, but it really hasn’t. I have a small amount of gold stocks I own as a hedge on the stock market. I can foresee wanting to use Crypto as a hedge on my gold hedge. I can easily see the rise of crypto and NFT’s as negatively hurting the price of gold. While crypto and NFT’s have no intrinsic value – gold is only a physical representation of an asset that has little intrinsic value. Its a complicated world.

As far as how I bought my Ethereum, I decided to go the easy way and buy it through PayPal – it was a very simple transaction. Crypto purists would say you really want to have your own wallet and store it off the grid, but I have such a tiny amount its not worth the hassle at this point. I guess if the apocalypse comes and we are bartering crypto currency, I may regret that decision.

For now, I am pretty much in watch and learn mode. This is a crazy investing world of late, and the inflow of the younger generations into investing is really challenging some long time strategies. Crypto may just be a bubble investment, or it might be the start of something big. Only time will tell.

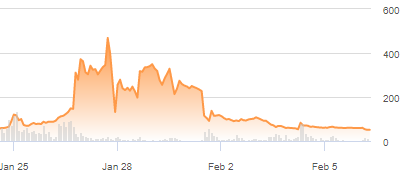

Lots has been written about the recent eruption of Gamestop stock as part of the Reddit rally against the big money on Wall Street, but I thought I would do a quick post just to sum up my thoughts. As you may recall, Gamestock stock went up 1000% after a Reddit Wall Street bets board focused small retail investors to buy Gamestop because it was shorted 140%.

Gamestop Stock Price

I think the initial strategy was correct – I think the fact that GME was shorted 140% was a mistake by the big money algorithm that failed to take that into account. When the reddit member who spotted that and spurred others via the forum to buy the stock was a creative way to profit off that mistake. I think those that got in on the first few days of the price move did pretty well. However, I think most the money that was made after January 26th was made by the big money hedge funds that the reddit movement was looking to punish.

A lot of the sentiment by the retail buyers was driven by hatred of the big money on wall street, and the feeling that the market is rigged against the small investor. To that point, I think it was a success. I think this exposed some tricks the big money used to kill the movement. While maybe Robinhood (the retail broker at the center of this) did have some fiscal reason to prevent traders on its platform from buying Gamestop stock during the heights of this movement, I find it hard to believe the big money behind Robinhood did not put pressure on the broker to keep retail investors from squeezing the shorts. This also brought to light the trade ‘front-running’ which pays for the ‘no-commission’ trades. When you trade a stock on a no-commission basis, it is clear the money is made up by the clearing house not giving you the best price. I also believe the expansion of the Gamestop trade to target other shorted stocks and silver was a deliberate diversion from the Gamestop movement.

The biggest fault I have with this is that it was driven by emotion. This anger at the big money should not of let investors to ignore basic stock fundamentals. One of the earliest lessons I learned (and keep trying not to repeat) is ‘don’t fall in love with a stock’. The mantra of ‘hold at all costs’ on Reddit is a failed strategy. This emotion is what let to all the small investors who joined the movement late to give their money to the hedge funds who know more about price fundamentals. While I don’t disagree with the sentiment on Reddit, I don’t think having thousands of small investors lose money on an irrational trade is the best response.

So that’s my take. I am heartened to see the younger generations take up these activist positions, and perhaps some good ideas came of this event. And I hope these small investors learned a little about mixing emotions with investing, and how important it is in most cases to keep them separated.

For years I have been working to eliminate emotion from investing, as I believe emotion causes bad decisions to be made. Anytime I look at an investment and decide I am holding it because I ‘hope‘ it will go up – indicates to me that emotion is entering into the decision process. In past posts I have referenced my investment model that I use to make investment decisions, and that has gone a long way towards using more analytics and less emotion when making decisions, but building an investing cadence has also helped.

Before I go too much into my investing process, let me digress and mention that some of my best investments have been made not using analytics, but using more thoughtful reasoning. Probably my two best stock investments ever were Microsoft in the early 90’s, and Amazon in the late 2000’s. Both of these stocks were ridiculously overpriced at the time and the analytics I used at that time would not support those investments. But I took a ‘gut level’ flyer on those because I reasoned out the long term trajectory of these companies (which my analytics tend to ignore) and took a flyer on these companies. I am sure there are examples of where this approach has burned me (and I conveniently erased those mistakes from memory), but I do think there are times where you have to look outside of analytics.

Over the years I have built a routine that helps me unemotionally make investment decisions that I share below – reasoning without emotion is still a critical factor.

My investment model attempts to predict which stocks will outperform the market in the following month. So I purposely rigged the model to unveil the next months predictions on the 20th of every month. So starting on the 20th, I look at my holdings, and compare them to projections, and make buy sell hold decisions to make over the next 10 days. I like to have my changes settled by the first of the month, so my portfolios reflect on the first of the month my plan for that month. This is important because at the start of the month I programmatically take a snapshot of my portfolios for performance measurement purposes. I try to limit my trades between the 1st and the 20th so that I can easily measure my performance metrics.

I think it is a positive to get away from trading for 20 days each month. I typically spend time during those periods researching investments, or making improvements to my investment model, or doing more creative thinking on investing in the future.

I have to admit though, I don’t get away from portfolio management completely during this time. Typically on the weekend, I will spend some time looking over my portfolio and filling in partial positions or trimming positions that might be too big. I try not to ever add new stock positions or sell out of positions during this time, I should always do that between the 20th and the 1st. But the nice thing about making some buy/sell decisions on the weekend is the market is closed. So on Monday morning, I can revisit those weekend decisions, and see if I Monday morning me agrees with weekend me.

I am fully aware more financial planners say it would be better to spend less time looking at your investments, and just buy and hold and let them grow organically. I would also recommend that for most investors; just buy low cost mutual funds and look a them quarterly/yearly. But for me, I can sleep better at night fully understanding my investments, and being fully accountable for my investment performance. If I find my approach underperforms my mutual fund benchmarks, I think I would throw in the towel and find something else to occupy my time. But if you are like me, and want to manage your investments, give some though to a routine that helps drive analytical decision making, and make sure you measure your performance.

I just completed an analysis of Zillow and Redfin, two companies that are competing to disrupt the real estate space. Valuing these companies presents a challenge, because neither currently are consistently profitable and are bloating their balance sheets with housing inventory. So I looked at visitor stats, which did provide an interesting way to compare the value of these companies. Both companies sell at a very high premium to the market, but I do believe long term both companies could be in interesting investment.

I have been building prediction modeling applications for years as a investor, as a way to try to identify when the various asset classes or particular stocks may be over or under priced. My current model is over 15 years old, and as you might guess is becoming a huge mess of code-spaghetti which is becoming difficult to modify.

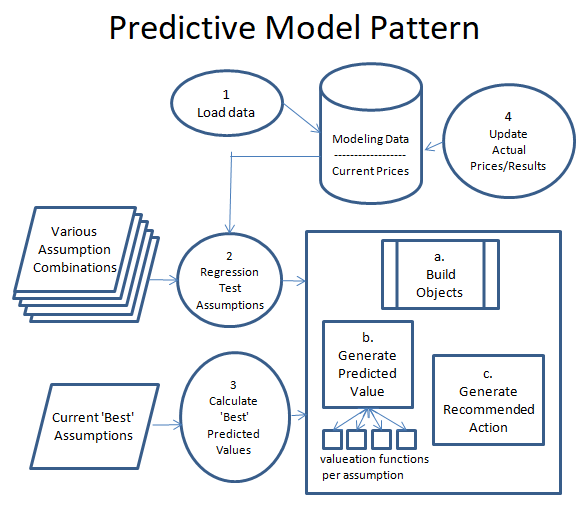

Recently, I stumbled across a full suite of college football data, and started to wonder if one could build a model to predict college football games. Rather than try to copy my existing investment model, I decided to mentally start from scratch and figure out the best way to design predictive models for maintainability. I now have a college football game prediction model up and running, using my new pattern I designed during this process:

Now this might be Data Science 101 to a data scientist, but this is not my area of expertise. My software suite is a SQL Server database and C#, tools I am very comfortable with. Rather than learn new tools and software specially built for data modeling, I thought it would be more interesting to design my own custom approach. I am a software developer, so my thinking how how to build this process was inspired my Model/View/Controller (MVC), a software design pattern that focuses on separation of logic for interconnected systems. So taking this foundation, I have broken the process of setting up an managing the model into 4 main components.

Create Program to Load Data. Before I build a model, I have to make sure I have access to the data necessary to power it. There are plenty of great API’s to gather investment data, and if necessary data can be gathered via data scraping. I have a good library of tools to call APIs, and a nice suite of data scraping tools. So building the logic usually takes some time, but the logic to gather the data can be nicely compartmentalized for easy maintenance.

Create Program to Regression Test Various Assumptions. Before building the program, you have to define a rough set of assumptions as to the cause and effects of various factors. The set of assumptions you create can only be limited by the data you have available. For example, for my College Football prediction model one assumption I tested was that a team is more valuable after a big home game loss. The assumption is the team might be more motivated to do well following a bad home loss, and potential betters are soured on the team. So you look at the data you have, then create various assumptions you can test against the data. Once you have a set of assumptions, you create a program to fire the assumptions at your prediction engine with varying the weight of each assumption each run. Doing this you hopefully identify assumptions that have no correlation to future performance, and ones that have a strong correlation or inverse correlation to future performance. Below I have expanded on how the prediction engine is built, as it is a core piece of the program.

Create Program to calculate the ‘best’ predictions. Once you have tested various factors against your historical data, choose the factors and weightings of each factor that performed best of all the factor combinations you fired at at the prediction engine. This will be what generates the predictions, then looks at the current price (or the current betting line in the case of my college football model), and determine the ‘best’ value prediction. Note that I plan to rerun my regression tests on this model quarterly, so that I can see how well the assumption weightings are holding up. If some start to deteriorate, I may adjust factors and weightings as appropriate.

Create Program to track predictions and update results. I think this is perhaps the most important piece. The prediction engine bases it’s prediction based on past data, so it is important to see if past data accurately predicts future results. So for example for the college football predictions, every Monday I run a job that updates the weekend scores, then compares the results to my predictions for the week. Each week I will look closer at the losses, to see what I missed, and maybe give me some ideas for additional factors to add. Of course, new factors may mean collecting more data, which further adds to the effort of building and maintaining the model. It is a very iterative process, as optimizations can always be made.

The Prediction Engine

Building the prediction engine is an iterative process in itself. The plan is to start small, then slowly add additional calculations over time. As long as additions are managed in an organized manner, the code base should be maintainable even after adding a large number of factors. The prediction engine (described in the big square in the diagram above) consists of 3 major parts.

a. Build Objects. The first thing to do when firing up the prediction engine is to pull the data stored in the database into a view model that exposes the data in a way to be easily accessible. These are typically complex objects that represent the entity you are making a prediction on (i.e. football game, a stock market security, asset class, etc.). For instance, a college football model would pull in a game object, which would have two teams attached to it with all the statistics and history needed for each team. For instance, a ‘bad previous week home team loss factor’ will require looking at past game performance in order to see if the a team had a bad loss in the previous week. As long as the data is there, that is a fairly simple subroutine to write.

b. Generate Predicted Value. Now that you have your data accessible – fire your list of assumption factors and weightings to calculate a value. To simplify the architecture of this, I have a separate subroutine for each factor calculation to try to avoid my logic bloat. This will allow me to isolate factors, and add new ones or delete invalid ones as necessary.

c. Generate Recommended action. Once you have calculated the value of all your assumptions against an object, you should have a score for that object. That score can then be compared to the price of the object to see if there is any action to be taken. For example, take a college football game, and given your assumptions and the data available step b came up with a calculation that the home team should win by 3 points. If the betting line has the home team favored by 14, and your threshold for action is a 7 point differential, then the recommendation action would be to place a bet on the visiting team. The same works for a stock market security. If step b calculates a stock price of $15, and the stock is priced at $10 the recommended action might be to buy the stock.

Note that it is also valuable to track the variability of the model in the form of standard deviation or R value. Some models may show a coorelation, but have a wide deviation. These deviations will help you set your ‘time to take action’ price. Typically the wider the deviation, the higher I set my action price.

Breaking the logic for this prediction engine into segmented parts should really help the management of the logic. In addition, I have a pretty good library of reusable logic components that I should be able to apply across multiple predictive models. My goal here is to slowly increase the size and scope of the calculations, while keeping the overall system pretty simple.

Now that I have my college football predictive model working, I will just continue to add assumptions to see if I can continue to increase the accuracy of my predictions. Then I will start tearing out components of my existing investment prediction engine, and rebuild it using this new model.

When will I be done with this project? Hopefully never. If all goes well, these models should be continually evolving and growing as more data is collected, and hopefully become more accurate.

For years I have held several bond funds, from corporate to high yield and international bonds, and I have been fairly satisfied with that low risk, low return portion of the portfolio.

As mentioned in a previous post, I am re-evaluating my allocation to bonds and bond funds, but I have also been experimenting with buying bonds directly rather than funds. It has been an interesting experience, and I thought it would be worth recapping a few points below.

High Yield Bonds. For years I have owned the Vanguard High Yield bond fund, which is probably the lowest cost high yield fund out there. Earlier this year, I reduced my allocation in high yield bonds, primarily because they tend to correlate more to the stock market than the bond market. Since my objective to buying bonds is to diversify from the stock market, that kind of defeats the purpose. However, as rates have fallen further and further, I decided to switch some of my corporate low-yield bond allocation to high yield, and take control of buying the bonds myself. The hope is I can get a little higher yield than just regular bonds, thus keeping the correlation with the stock market lower. High yield bond funds typically have a huge allocation to energy stocks, which in this environment I also want to stay away from. So I have been building a portfolio of reasonable quality short term maturities that are technically high yield, but I expect will behave more like bonds. I have bought bonds issued by companies such as T-Mobile, Netflix, Best Buy, and Lennar Corp which I feel pretty comfortable owning. Of course, I sacrifice yield for this, but I do feel better owning bonds in companies I understand.

TIPS. I can’t do a post on bonds without mentioning TIPS – Treasury Inflation protected securities. TIPS are issued by the Federal government and the interest rate is pegged to the inflation rate. These rates naturally are very low.. but then what isn’t? My recommendation for anybody considering TIPs is to make sure and buy I-Bonds from treasurydirect.gov first. The government limits the purchase of I-Bonds to $10,000 per Social security number. The current composite rate for I-Bonds is 1.06% which in most worlds is terrible. However, you can withdraw them penalty free after 5 years (so effectively a 5 year maturity), plus you get inflation protection. In past years there has been a fixed component to the rate, so it was even a better deal, but the current rate is still above a 5 year CD rate, and if inflation increases, you will do even better. And you know the Fed is trying everything it can to increase inflation.

Foreign Bonds. I have foreign bond funds, and I was considering starting to allocate to owning individual foreign bonds. So I started by looking at the holdings in the Vanguard Emerging Market Bond ETF. This fund has a yield of 3.89%, which is nice in this environment. However, the average maturity is pretty high at 13+ years, which is way longer than I would typically buy a bond for (who knows what he world will look like in 13 years?). It then occurred to me that I have no strong feeling about which countries are over or under priced. I also looked at the market value they had listed for some of their bonds, and looked at the price I could buy the bond for, and in most cases their listed price was about 1% cheaper than I can buy the bond for. I am pretty leery about bond spreads, especially when rates are so low – a 1% spread is in many cases one years worth of interest. So for now, I think I will continue to buy foreign bonds thru funds, as I don’t think I can outperform the experts by 1%.

My foray into holding individual bonds has been interesting, and it makes me feel better when I understand what I own. That is probably the biggest benefit to buying bonds outright. Even if I was a bond wizard I don’t think I can win big holding bonds vs funds. The biggest benefit is probably education and learning about how the bond market works.

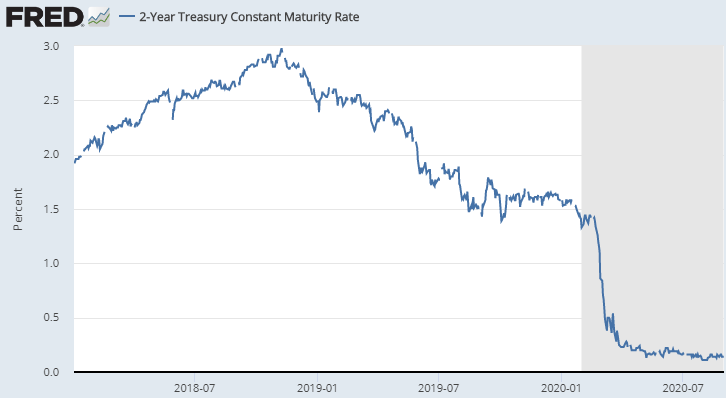

The craziness of markets over the last few months caused by the Coronavirus have been incredible. As in investor, I am trying to forecast where we go from here, and what are the best and worst possible outcomes. While the stock market and its disconnect from the economy seems to be getting most of the headlines, I think the bigger story is the bond market and where it goes from here.

As seen in the chart above, the 2 year treasury bond has dropped from near 3.00% in late 2018 to 0.13% in September of 2020. This, along with the government’s fiscal stimulus is probably most responsible for the stock market’s disconnect from the economy.

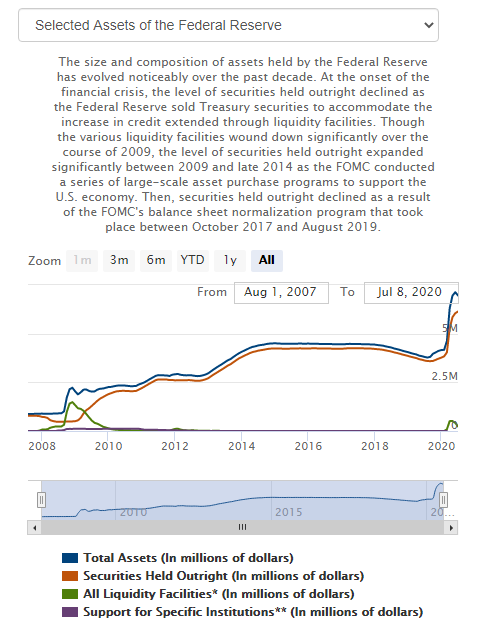

The stimulus here is unprecedented – dwarfing the financial crisis of 2009:

The stock market is fueled by stimulus, and seems to be signalling full speed ahead. Given the government intervention, it is nearly impossible to determine if the market is overvalued or undervalued, as the economy is a secondary factor to stimulus.

I also think the stock market is being fueled by Bond investors jumping ship. Risk averse bond investors not reinvesting bonds that mature at .14% – instead invest in Apple or Microsoft that has a growing yield and is ‘safe’. I understand the appeal of this strategy, but at these prices it seems like a lot or risk is being taken on out of desperation.

At any rate, one almost sure bet is that the bond market will be a loser. This bet does assume that the aversion to negative interest rates in the US will persist. Given that assumption, the best case for the investors in 2 year treasuries would be a no inflation or deflationary economy, with rates at or near zero. Given that assumption, the rate of return on bonds is still near zero.

The worst case scenario for bond investors is all this stimulus in the hands of consumers, combined with an economy waking from the COVID shutdown, leads to inflation. The only hope the government has of reducing the debt is to increase inflation, and so those in charge of the money press are incented to cause some inflation. The government has targeted and pretty much achieved a 2% inflation rate for the last few years. The Federal Reserve recently adjusted its inflation mandate to declare they may allow overshooting their 2% target rate – a further sign of inflation in the medium to long term. This does not bode well for a T-Bill yielding .14%.

So what to do with my bond portfolio. My asset allocation currently has a percentage in US Bonds, and if I am to reduce that allocation, where to I put it? Lots of options, but none that I really like:

Increase Allocation to the stock market. One option is to increase allocation to the stock market- maybe in the ‘bond proxy’ sectors. Options such as Utilities and Financials (JP Morgan is yielding over 3.6%%, and the government won’t let anything happen to that bank. Most local and regional ‘safe’ utilities yield in the 2-4 % range. Other options might be focusing on reasonable yielding low valuation stocks. Rocky Brands comes to mind with a near 2% yield and Price/Book around 1, P/E of 9, and a little growth. Many bond investors have already flocked to the market and these sectors, so it may be too late here to buy these possibly inflated assets. Definitely adding risk with this strategy.

Increase Allocation to Gold. I have an allocation in gold already, though I hate the idea of holding rocks in my portfolio. But the way the world if printing money, Gold has had a pretty good year and the money printing wont be stopping anytime soon. I have been experimenting with buying quality Gold miners, then selling covered calls in the +10% range which generates pretty good income. This is still an experimental strategy, but it seems to be doing no worse than just holding gold (via BAR) and gold mining stocks, and makes me feel better about holding this asset class.

Increase Allocation to TIPS (Treasury Inflation Protection Securities). An interesting play here – TIPS are pegged to the inflation rate – so if inflation does hit, your interest rate increases. If we have deflation, yields will turn negative (unless you buy IBonds via Treasury Direct – which have a floor of 0% rate – but there is a limit on annual purchases). Probably worth taking your chances with TIPS over fixed rate bonds, The Vanguard TIPS Mutual Fund is currently yielding over 2%, so that might be an interesting option, but its not going to make you rich. Its also moved up alot over the last few months, as other people have figured this out several months ago.

Increase Allocation to Real Estate/REITs. This is my least favorite diversification play. In volatile times, REITs move more like stocks than bonds, so its a huge risk increase to move from bonds to economy dependant real estate. There are certain areas of REITs that my be interesting for ‘safer’ diversification (i.e. farmland REITs), but historically they haven’t performed well. I also believe the fallout from COVID has yet to be reflected in the commercial REITS.

I am not alone facing these choices – most investors saving for retirement or in retirement are facing this dilemma. Right now I am leaning toward increasing my allocations to the stock market – but really emphasizing low P/E or low Price to Book stocks in defensive sectors that haven’t participated in this recent tech bubble run-up. Those stocks are out there, it just requires some digging.

Rocky Brands is an interesting story – one would think they would be hit pretty hard during the pandemic. They were expected to lose $0.16 a share in Q2, instead they reported a $0.33 gain on unexpected demand.

An interesting conservative buy at these levels and in this environment.